How Pension Tax Relief Works in the UK, in Plain English

Pension tax relief is the closest thing the UK government offers to free money for your retirement. For every pound you put into a pension, the government adds extra on top to compensate for the income tax you paid on that pound. And most people either don't understand it, don't claim all of it, or don't realise how much it's worth.

This article explains pension tax relief in the simplest terms possible: how it works, how much you get, how to claim it, and the mistakes that cost people money every year.

What pension tax relief actually is

When you earn money, the government takes income tax before you see it. Pension tax relief reverses that. It gives the tax back when you put money into a pension.

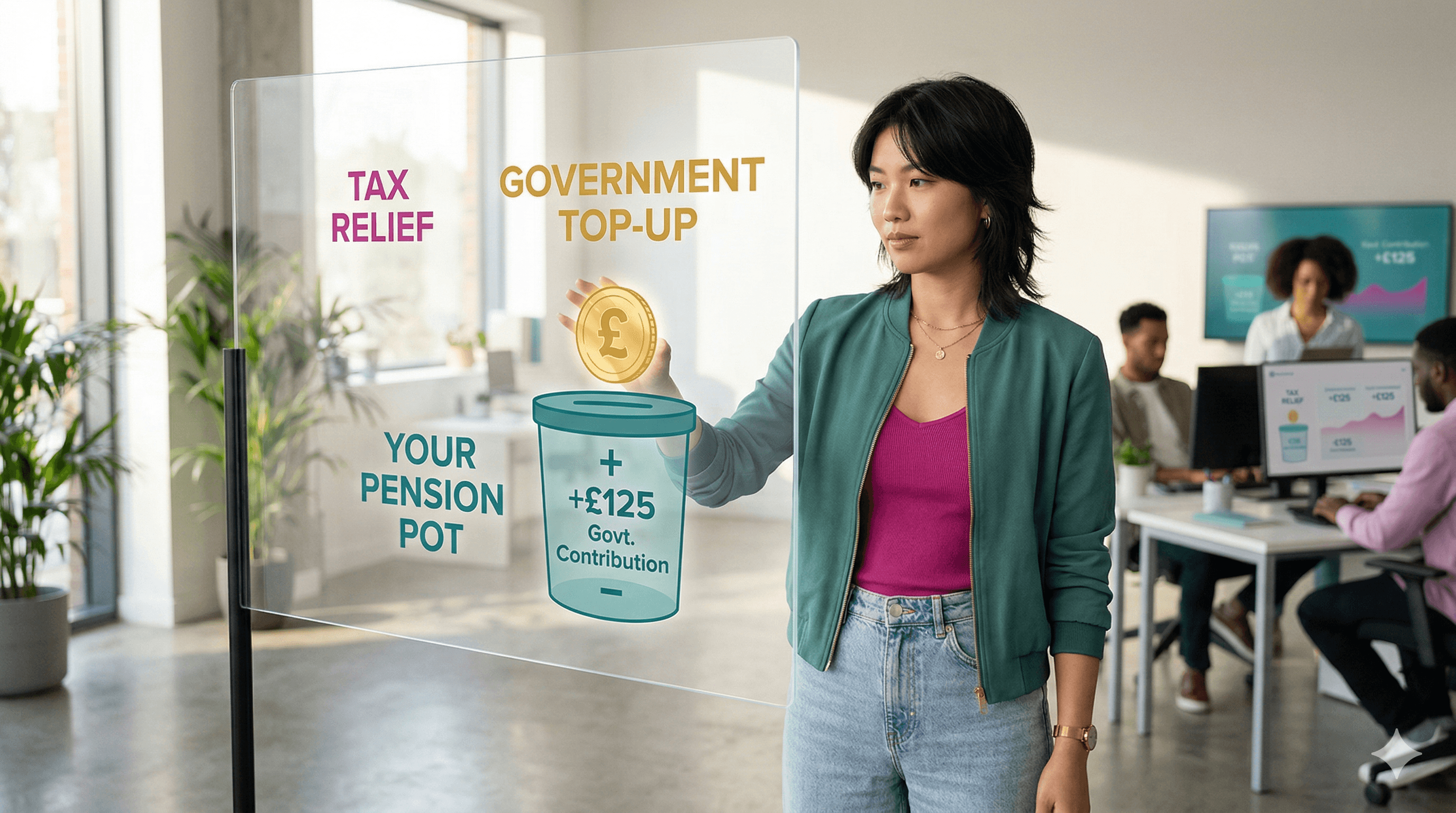

If you're a basic-rate taxpayer (20%) and you put £80 into a pension, the government adds £20 of tax relief, bringing the total contribution to £100. You put in £80 and got £100 working for your retirement. That's a 25% instant return before any investment growth.

If you're a higher-rate taxpayer (40%), you can claim an extra £20 back through your tax return, meaning that same £100 in your pension only cost you £60 out of pocket. That's a 67% boost.

If you're an additional-rate taxpayer (45%), the effective cost drops to £55 for every £100 in the pension.

The government is giving you back the tax you paid on your earnings, as long as you agree to put that money away for retirement.

How the two methods work

There are two systems for delivering pension tax relief in the UK. Which one you're on depends on how your pension is set up.

1. Relief at source

This is how most personal pensions, SIPPs and some workplace schemes work. You contribute from your take-home (after-tax) pay. The pension provider claims the basic-rate tax relief (20%) from HMRC and adds it to your pot automatically.

You put in £80. Your provider claims £20 from HMRC. Your pension gets £100.

If you're a higher or additional-rate taxpayer, you need to claim the extra relief yourself through your Self Assessment tax return (or by calling HMRC to adjust your tax code). This is the bit most people forget.

2. Net pay (salary sacrifice)

This is how many employer workplace pension schemes work. Your contribution is taken from your salary before tax is calculated. So you never pay tax on that money in the first place.

If you earn £3,000 a month and contribute £200 via net pay, you're only taxed on £2,800. The full £200 goes into your pension with tax relief already baked in.

Under net pay, there's nothing extra to claim. All the relief happens automatically. You also save on National Insurance contributions, which is a bonus that relief-at-source schemes don't provide.

How much tax relief can you get?

You can get tax relief on pension contributions up to 100% of your annual earnings or the annual allowance (currently £60,000 in 2026/27), whichever is lower.

If you earn £35,000 a year, you can contribute up to £35,000 and receive tax relief on the full amount. If you earn £80,000, the cap is the £60,000 annual allowance.

There are a few exceptions:

Carry forward: if you didn't use your full annual allowance in the previous three tax years, you can carry the unused amount forward to this year. This is useful for one-off large contributions, like after a bonus or inheritance.

Tapered annual allowance: if you earn over £260,000 (adjusted income), your annual allowance is gradually reduced, down to a minimum of £10,000.

Non-earners: even if you have no earnings, you can contribute up to £2,880 a year and receive £720 in tax relief (bringing the total to £3,600). This is worth knowing for stay-at-home parents.

The higher-rate claim most people miss

If you're a higher-rate taxpayer contributing to a relief-at-source pension, the provider only claims the basic 20% from HMRC. You have to claim the other 20% yourself.

You can do this by:

Filling in a Self Assessment tax return (box for pension contributions), or

Calling HMRC and asking them to adjust your tax code so you get the relief spread across the year through your salary.

HMRC estimates that hundreds of millions of pounds in higher-rate relief goes unclaimed every year because people simply don't know they need to ask. If you've been a higher-rate taxpayer and haven't claimed, you can go back four tax years.

If you pay 40% tax and contribute to a personal pension, you are almost certainly owed money. Check.

What about employer contributions?

When your employer contributes to your pension, those contributions don't come out of your salary, so there's no tax to relieve. Employer contributions are a business expense for them and are not counted against your personal tax relief.

However, employer contributions do count toward the £60,000 annual allowance. So if your employer puts in £30,000 and you put in £30,000, you've hit the cap.

When you take the money out

There's a trade-off. You get tax relief going in, but you pay income tax when you take money out of your pension (from age 55, rising to 57 in 2028). The first 25% of your pension is tax-free. The rest is taxed as income.

For most people, this is still a good deal because you're likely to be on a lower tax rate in retirement than during your working years. A 40% taxpayer who retires on a 20% income gets full relief at 40% going in and only pays 20% coming out.

Common doubts

"Do I get tax relief on my workplace pension?" Yes. It's either applied automatically (net pay) or claimed by your provider (relief at source). Check your payslip to see which method your scheme uses.

"What if I'm self-employed?" You can contribute to a SIPP and claim tax relief exactly the same way. The provider adds 20% automatically, and you claim the rest via Self Assessment.

"Is there a lifetime limit?" The Lifetime Allowance was abolished in April 2024. There's no longer a cap on how much you can hold in your pension. The annual allowance (£60,000) is the main constraint.

"Can I get tax relief on contributions to my spouse's pension?" Not directly. But your spouse can contribute to their own pension (up to £2,880 net, topped to £3,600) even if they have no earnings.

"What if I accidentally contribute too much?" You'll face an annual allowance charge on the excess. The charge is at your marginal tax rate, effectively removing the tax relief. Your pension provider can help you sort this out.

Where Mona fits

Mona helps you track your pension contributions against the annual allowance, flags when you might have unclaimed higher-rate relief, and reminds you before the tax year ends if you have unused space to fill. She connects to your bank via Open Banking so you can see exactly how much room you have left and how much you've already contributed across all your pensions.

This article is for education only and is not financial advice. For free, impartial guidance on pension tax relief, MoneyHelper.org.uk (run by the UK government's Money and Pensions Service) and gov.uk/tax-on-your-private-pension/pension-tax-relief are the best starting points.

The bottom line

Pension tax relief means every pound you put into a pension costs you less than a pound. Basic-rate taxpayers get a 25% boost automatically. Higher and additional-rate taxpayers get even more, but they have to claim it. The annual allowance is £60,000, and unused allowance can be carried forward three years.

It's one of the most valuable benefits in the UK tax system, and most people leave money on the table.

Tax relief turns your pension from a good idea into a no-brainer.

Check your payslip to see if your workplace pension uses relief at source or net pay. If you're a higher-rate taxpayer on relief at source, call HMRC or file Self Assessment to claim back the extra 20%. Do this today if you haven't already.