Joint Savings Accounts: How They Work and When to Use One

Saving together can strengthen relationships and accelerate shared goals, but the legal and financial implications mean you need to think carefully before combining your money. We'll walk you through what joint savings accounts actually are, when they make sense, and the tough conversations worth having first.

How do joint savings accounts work in the UK?

A joint savings account is owned by two people with equal legal rights. Both account holders can access the full balance, make deposits, and withdraw money whenever they want - neither person needs permission from the other. The account is in both names, and both of you receive statements.

This sounds convenient, and it can be. But that 'equal access' rule is the core tension: if you put in £5,000 and your partner puts in £1,000, you both legally own all £6,000. If they withdraw the lot, that's their right. From the bank's perspective, they can't referee ownership disputes - the law treats it as shared property.

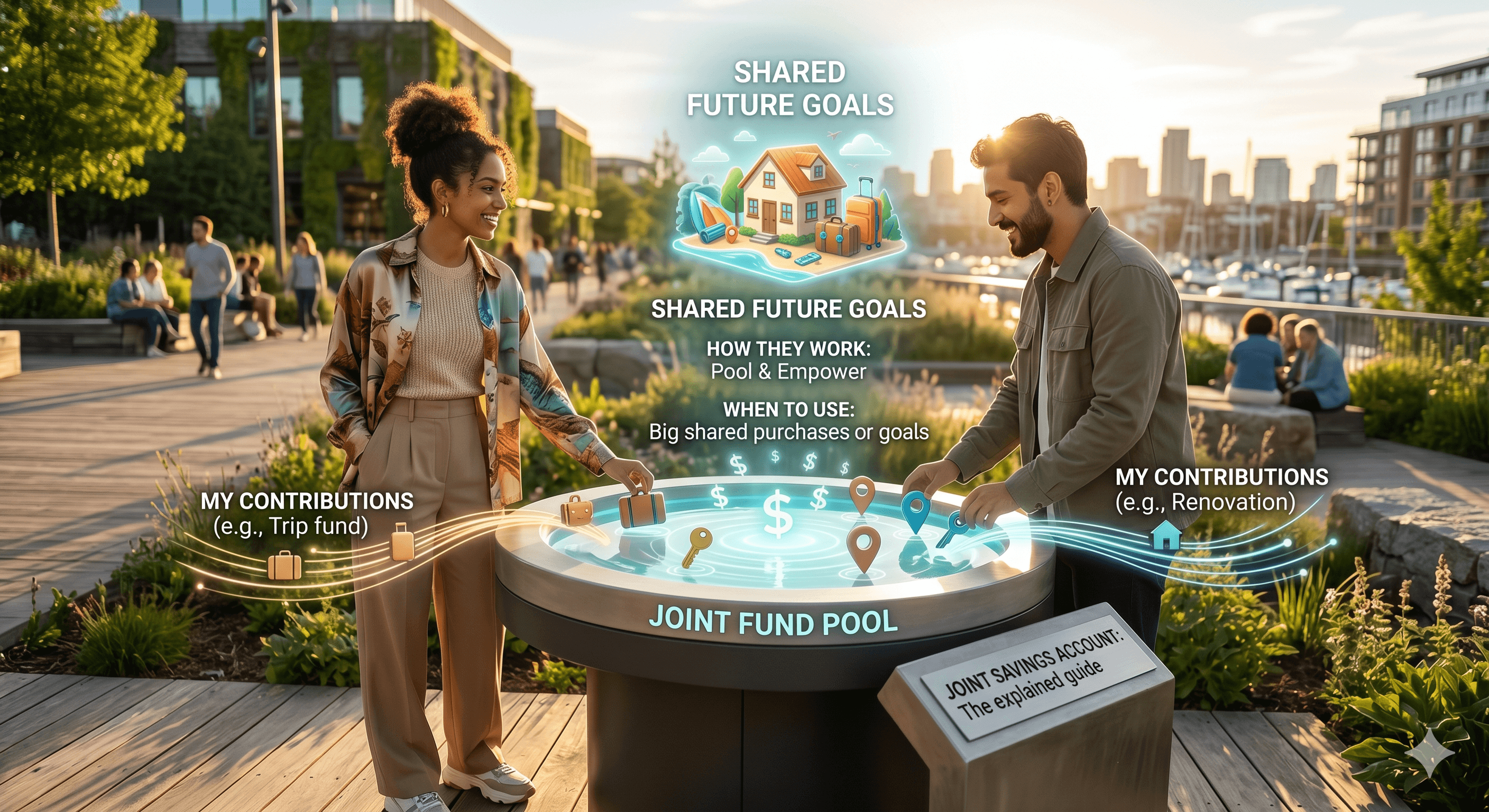

When should you open a joint account instead of keeping things separate?

Joint accounts work best when you're pooling money for a clear, genuinely shared purpose. Couples saving for a deposit on a house together, business partners setting aside funds for equipment, or parents and adult children saving for a family holiday - these are situations where both parties are equally invested and equally contributing.

They make less sense if you're simply combining accounts for convenience. Many couples manage perfectly well with separate accounts and a shared account just for joint expenses. Couples in the early stages of a relationship, or those wanting to maintain financial independence, typically fare better keeping personal savings separate.

What are the legal implications of opening a joint account?

The key legal principle is that a joint savings account creates what's called 'joint ownership' - money in the account isn't divided between you by contribution, it's all legally owned by both of you together. This matters for several reasons.

If you die, money in a joint savings account passes automatically to the surviving owner - it bypasses your will. That's useful in some cases, a problem in others. If you're in a relationship where you want to leave money to other family members or charities, this automatic transfer might not align with your wishes. Also, if you're receiving benefits like Universal Credit or Pension Credit, a joint savings account counts as shared capital, which could affect what you're entitled to receive.

What happens to a joint account if the relationship ends?

This is where things get complicated. If you were married or in a civil partnership, a joint account is usually treated as a shared asset during divorce or dissolution proceedings. The court will likely consider it part of the overall marital assets to be divided fairly - though 'fairly' doesn't always mean 50-50.

If you're in an unmarried relationship, the law is less clear. Both of you have equal legal claim to the full balance. That means your former partner could theoretically withdraw everything, and you'd have to pursue a court claim to recover your share. This is a real risk. If you think a relationship might end, a joint account is dangerous for protecting your money.

Once a relationship ends, contact your bank immediately to discuss freezing the account or restructuring it. Don't assume your ex will act reasonably.

How do you open a joint savings account?

The process is straightforward: both of you need to visit a branch or apply online together with the bank's app or website. You'll need proof of identity for both account holders - a passport or driving licence - and proof of address for both people (a recent utility bill or council tax letter works).

Banks do conduct affordability and creditworthiness checks on both applicants. If either of you has a poor credit history, you might be declined. Some banks have strict joint account policies - they may ask about your relationship, your purpose for opening the account, or require both signatures on all paperwork.

Once opened, ask the bank how it handles account access. Most allow either person to manage it online or in branch. Make sure you both know how to access your statements and set up alerts so you're both aware of withdrawals.

What are the real advantages of a joint account?

Beyond the obvious convenience, a joint account creates transparency and shared accountability. If you're saving for a deposit together, seeing that pot grow in a single account can be motivating. There's no faffing about with transfers between accounts or trying to remember how much each person has contributed.

If either of you becomes seriously ill or incapacitated, the other has immediate access to money for household bills or medical expenses - you don't need to wait for power of attorney paperwork to be processed.

Financially, some joint accounts offer better interest rates, though this isn't always the case. It's worth comparing rates before committing.

What are the real disadvantages and risks?

Loss of financial control is the biggest one. You're trusting the other person not to empty the account. If your relationship breaks down or they're financially irresponsible, that trust becomes risky. There's also the problem of blurred boundaries - if you have separate accounts and a joint account, managing finances becomes more confusing, not simpler.

If either of you racks up serious debt, creditors may be able to pursue the joint account. It's not automatic, but a joint account is viewed as shared property, which makes it a potential target. Benefits payments can be affected too - as mentioned, joint savings count towards capital limits on means-tested benefits.

There's also the divorce risk. If you put money into a joint account during a marriage or civil partnership, you may struggle to prove it was yours before you put it in. The account itself is treated as a shared asset.

What conversations should you have before opening one?

First: discuss what happens if the relationship ends. How would you split money in the account? If you can't agree on this before opening it, don't open it. Second: clarify the purpose. Is this for a specific goal with a timeline, or indefinite joint saving? That affects how you'll manage it.

Third: talk about withdrawals and transparency. Will you tell each other about big withdrawals? Will you need joint consent for amounts over a certain limit? These might sound unromantic, but they prevent resentment. Fourth: discuss what happens if one person dies - have you made a will that reflects your wishes, or are you comfortable with automatic transfer to the surviving partner?

Finally: check the impact on benefits, tax, and other financial arrangements. If either of you receives means-tested benefits, opening a joint account could affect your entitlement.

Where Mona Fits

Mona makes it simple to find and compare savings accounts that suit your needs - whether joint or individual. You'll get a clear view of interest rates, access terms, and features across UK providers. If you're splitting bills with a partner but want to keep personal savings separate, Mona helps you find the right mix of accounts so your money works as hard as it can.

The Bottom Line

Joint savings accounts are powerful tools for couples working toward shared goals, but they carry real legal and financial risks if things go wrong. They only make sense when you're genuinely aligned on the purpose, you trust each other completely, and you've thought through what happens if circumstances change. If you're unsure, keeping separate savings accounts and using a joint account just for shared expenses is often the smarter choice.

Ready to find the right savings account for your situation? Use Mona to compare rates and features tailored to your needs.

For impartial financial guidance on joint accounts and savings, visit MoneyHelper.org.uk - it's backed by the UK government and completely free.